Aerospace: Revenue $1.825B (-12.0% YoY); EBIT $346m (-21.2% YoY)

Combat Systems: Revenue $1.44B (+11.9%); EBIT $224m (+9.3% YoY)

Information Systems and Technology: Revenue $2.236B (+4.2% YoY); EBIT $247m (+4.7% YoY)

Marine Systems: Revenue $2.034B (+5.2% YoY); EBIT $184m (+14.3% YoY)

StrengthsGeneral Dynamics (NYSE:GD) has a strong market positioning. The increase in military budget under the Trump administration has been beneficial industry-wide. In February 2018, the U.S. Navy submitted a budget request of $194.1B, as part of the broader fiscal 2019 defence budget worth $716B. The submission includes a $58.5B procurement budget for purchasing 10 new ships, including two submarines, and 54 ships across the Future Years Defence Plan (FYDP). General Dynamics, being one of the only two contractors in the world equipped to build nuclear-powered submarines and a prime military shipbuilder, is expected to benefit from the increased budget.

Outside the US, GD also has a robust pipeline in Europe and the Middle East. Moreover, Asia-Pacific has recently emerged as a region for increased demand for defence equipments, as developing countries step up procurement efforts, thereby offering enhanced expansion option for defence contractors.

During the first quarter of 2018, the company��s European-based business witnessed a solid order activity throughout Europe and into parts of Africa. Notably, General Dynamics�� military vehicle production revenue increased substantially in the reported quarter driven by the ramp up of several international production programs, including U.K. AJAX armoured fighting vehicles, Romanian Piranha 5-wheeled armoured vehicles and the upgrade of LAVs for the Government of Canada.

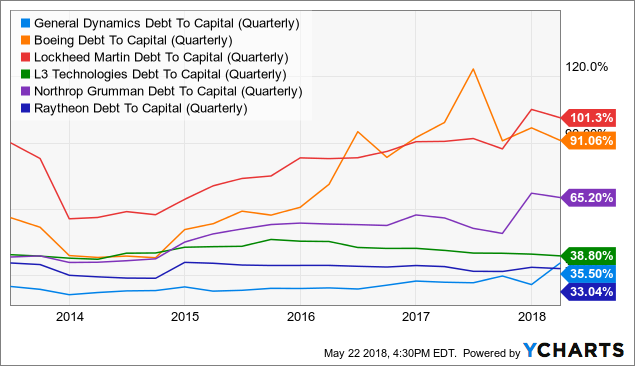

The balance sheet strength of the company remains robust, with a debt-to-capital ratio at the lower end of the industry spectrum (see chart below). This implies a larger possible borrowing capacity for the company, no matter for internal restructuring or further acquiring subcontractors to enhance its supply chain. Therefore, the company is in a competitive position among its peers to generate positive revenue and profit growth.

GD Debt To Capital (Quarterly) data by YCharts

GD Debt To Capital (Quarterly) data by YCharts

The company operates in a highly competitive market. There has been a growing trend of specialisation within the industry (e.g. Boeing (BA) in missile systems (ICBMs), Lockheed Martin (LMT) in jet fighters, L3 (LLL) in communications, Northrop Grumman (NOC) in UAS and back-end missile systems, Raytheon (RTN) in front-end missile systems and communications). This could have a negative impact to more diversified contractors like GD, as the competitive advantage of the other contractors might tighten contract margins.

The company is tightly correlated to the cyclical aerospace market, which is currently in a recovery phase. However, with rising Treasury yields and tightening market risk premiums, the general market seems to be pricing in a correction in late 2018 or early 2019. Moreover, the company's share price may be highly event-driven at times and highly sensitive to geopolitics. The gradual thawing tensions in Korea and uncertainty over the Middle East pose as downside risks. Also, the company��s dependence on international sales for a significant portion of its revenue exposes it to currency risks and other geo-political risks.

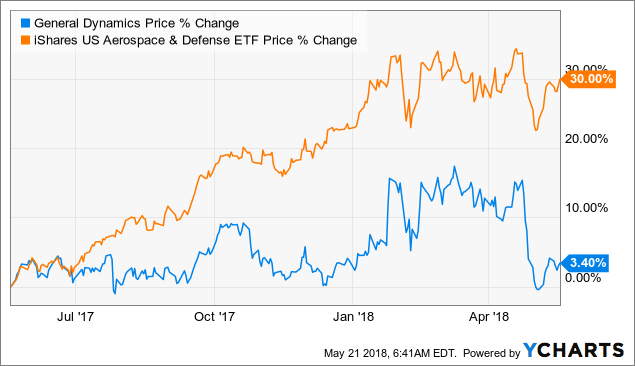

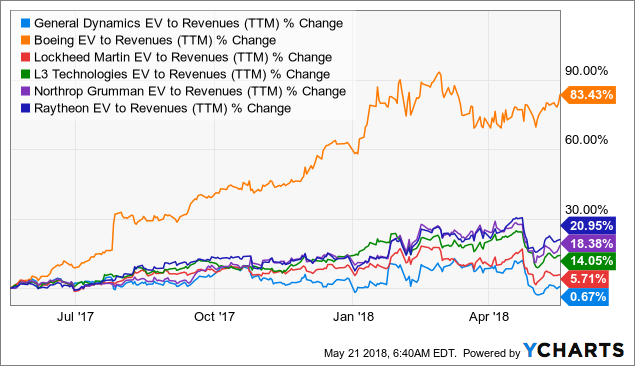

General Dynamics�� share price has underperformed the broader market over the last twelve months. The company's share price has gained 3.4% compared with the broader industry��s 30% rally (see chart 1 below). GD's historical EV/revenue ratio (see chart 2 below) reflects the fact that investor sentiment is not consistent with the industry-wide upward trend, despite relatively flat revenue growth. There is also a possible substitution bias from investors towards the other defence contractors (notably Boeing, Lockheed Martin, Northrop Grumman and Raytheon) that have shown better operating results and growth drivers.

GD data by YCharts

GD data by YCharts GD EV to Revenues (TTM) data by YCharts

GD EV to Revenues (TTM) data by YCharts

On Apr 3, 2018, General Dynamics completed its acquisition of CSRA Inc. for $9.7 billion. CSRA has been integrated into General Dynamics Information Technology (GDIT), which in turn has created a premier provider of high-tech IT solutions to the government IT market. The acquisition strengthens GDIT's competitive advantage and consequently, we may expect General Dynamics to secure more government IT contracts. Impressively, the takeover is projected to add approximately $3.6 billion of revenue in 2018 to the company��s Information Systems and Technology (IS&T) group��s revenue, which is already the largest operating segment.

Moreover, on Apr 11, 2018, General Dynamics announced that it has entered into a binding agreement to acquire Hawker Pacific, a leading provider of integrated aviation solutions across Asia Pacific and the Middle East, for $250 million. This deal is likely to enable the company provide its Gulfstream services in places where it does not have standalone Gulfstream support facilities. This would streamline and consolidate the supply chain, thereby boosting revenue growth and profitability margins, of GD's Aerospace segment, which has been lagging relatively to the company's other operating segments.

Lastly, the G500 and G600 jets have made significant progress in launching to the commercial market. GD has recently begun the last phase of flight testing for its G500 aircraft. After 300-hour function and reliability testing, the programme will then be pending final document approval by the FAA. GD will begin pilot training with FlightSafety in August and commence deliveries later this year, expecting to duly meet its 2018 G500 planned customer deliveries. The G600 is benefiting from all of these efforts and will wrap up its certification in the second half of 2018. The company aims at beginning deliveries of the G600 jet in 2019.

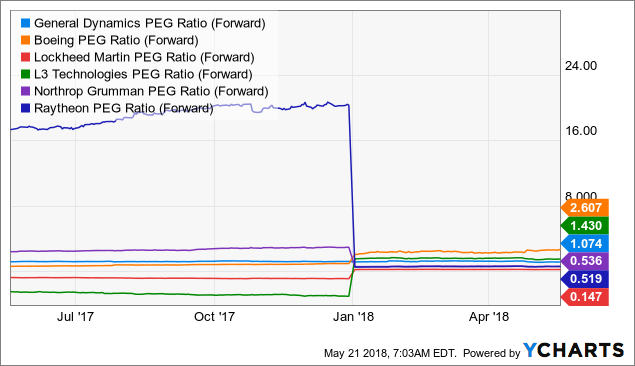

Investment ThesisEven though the flat change in valuations relative to peers might signal negative investor sentiment, we do see it as a possible value opportunity to enter the market, as there are positive growth drivers towards the business, in particular the recent acquisitions of CSRA and Hawker Pacific. The fundamentals and growth outlook are also robust, while the market has adequately priced the growth prospects (see chart below).

GD PEG Ratio (Forward) data by YCharts

GD PEG Ratio (Forward) data by YCharts

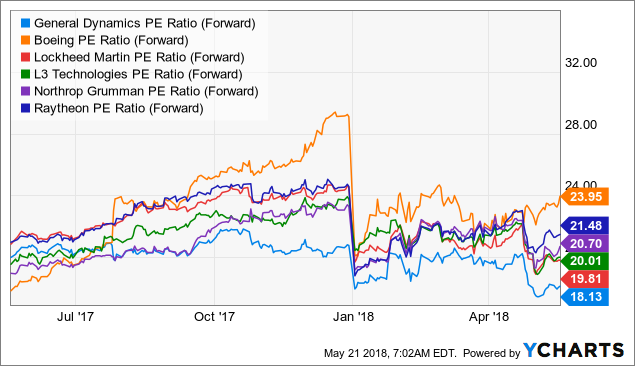

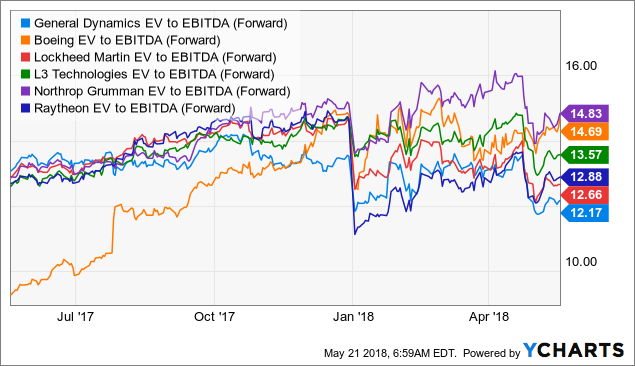

Looking at more straightforward fundamental ratios, GD remains at the lower end of the multiples spectrum.

GD PE Ratio (Forward) data by YCharts

GD PE Ratio (Forward) data by YCharts GD EV to EBITDA (Forward) data by YCharts

GD EV to EBITDA (Forward) data by YCharts

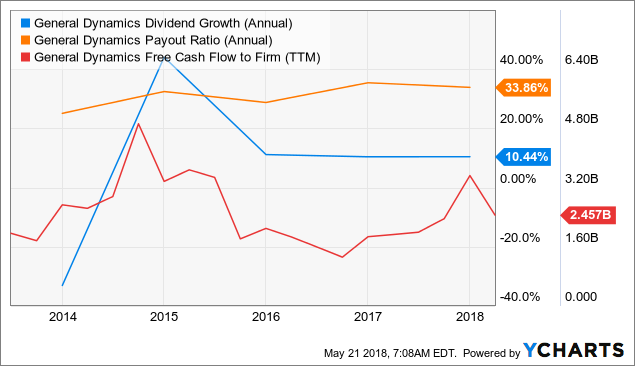

Furthermore, dividend growth remains robust and forward dividends remain robust and consistent.

GD Dividend Growth (Annual) data by YCharts

GD Dividend Growth (Annual) data by YCharts

Our target price for General Dynamics is $220, implying a P/E of 20.75x and EV/EBITDA of 13.52x. The target price is based on a cash flow forecast model. The short-term outlook is Overweight, but mid- to long-term outlook is Neutral. The valuation still slightly lags behind the respective industry averages of 26.20x and 13.88x, but the growth prospects of GD is not as lucrative as its peers, hence the neutral long-term outlook.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment